FOX : Báo cáo phân tích công ty - Khuyến nghị Mua

Source: MBS

Report type: Phân tích Doanh nghiệp

Publish date: 01/13/2017

Download count: 652

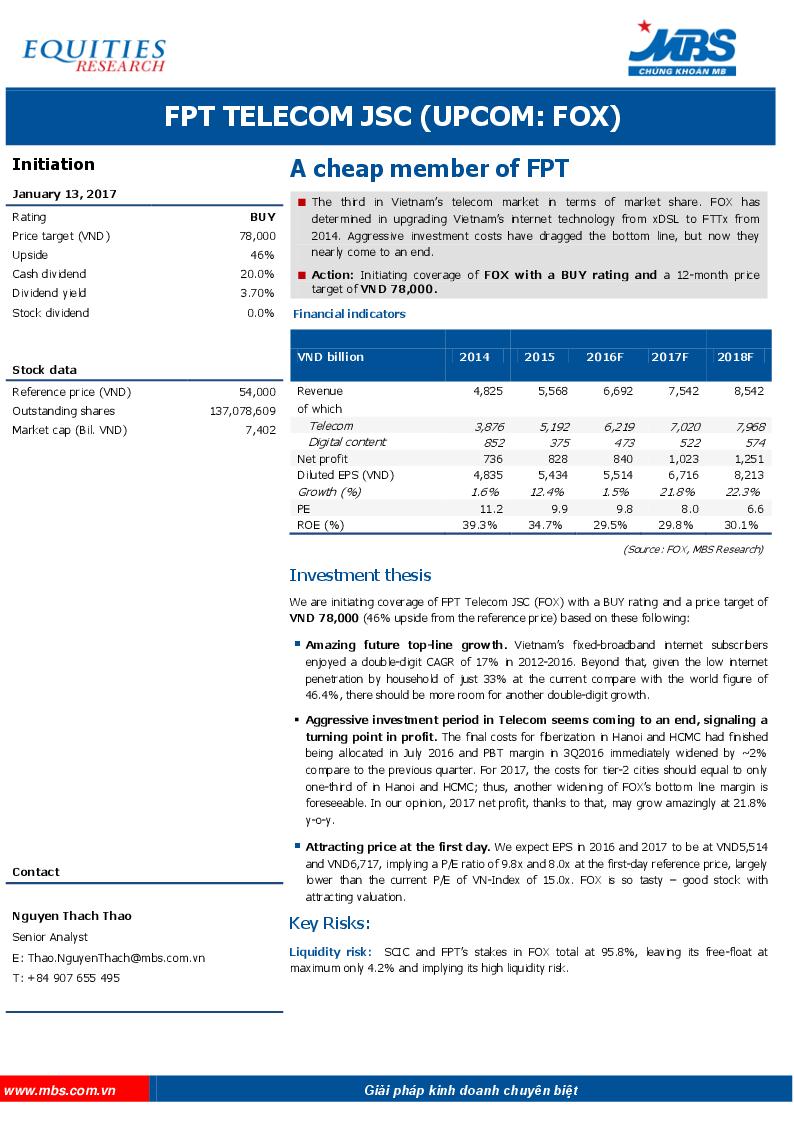

Investment thesis We are initiating coverage of FPT Telecom JSC (FOX) with a BUY rating and a price target of VND 78,000 (46% upside from the reference price) based on these following: Amazing future top-line growth. Vietnam’s fixed-broadband internet subscribers enjoyed a double-digit CAGR of 17% in 2012-2016. Beyond that, given the low internet penetration by household of just 33% at the current compare with the world figure of 46.4%, there should be more room for another double-digit growth. Aggressive investment period in Telecom seems coming to an end, signaling a turning point in profit. The final costs for fiberization in Hanoi and HCMC had finished being allocated in July 2016 and PBT margin in 3Q2016 immediately widened by ~2% compare to the previous quarter. For 2017, the costs for tier-2 cities should equal to only one-third of in Hanoi and HCMC; thus, another widening of FOX’s bottom line margin is foreseeable. In our opinion, 2017 net profit, thanks to that, may grow amazingly at 21.8% y-o-y. Attracting price at the first day. We expect EPS in 2016 and 2017 to be at VND5,514 and VND6,717, implying a P/E ratio of 9.8x and 8.0x at the first-day reference price, largely lower than the current P/E of VN-Index of 15.0x. FOX is so tasty – good stock with attracting valuation.

Latest report

Khuyến cáo: Các báo cáo phân tích được Vietstock phân tích hoặc thu thập từ những nguồn tin cậy. Tuy nhiên tất cả các quan điểm, luận điểm, khuyến nghị mua/bán trong báo cáo chỉ mang tính tham khảo. Vietstock không chịu trách nhiệm đối với bất kỳ khoản thua lỗ từ đầu tư nào do sử dụng các báo cáo phân tích này.

Search

| Vietstock: Research - Analysis |

| Macro - Market strategy |

| Sector Analysis |

| Business Analysis |

| References |

| Enterprise introduction |

| 05/02/2024 | Thị trường chứng quyền 03/05/2024: Tình hình đang chuyển biến tích cực hơn |

| 05/02/2024 | Chứng khoán phái sinh ngày 03/05/2024: Tâm lý thận trọng vẫn còn sau kỳ nghỉ lễ |

| 05/02/2024 | Vietstock Daily 03/05/2024: Tăng trong thận trọng |

| 05/02/2024 | Nhịp đập Thị trường 02/05: VN-Index bứt phá cuối ngày, khối ngoại lại tạo mối lo |

| 05/02/2024 | Phân tích kỹ thuật phiên chiều 02/05: Trạng thái giằng co chi phối thị trường |

| 05/02/2024 | Tuần 02-03/05/2024: 10 cổ phiếu nóng dưới góc nhìn PTKT của Vietstock |

| 05/01/2024 | Thị trường chứng quyền tuần 02-03/05/2024: Hiện tượng phân hóa vẫn còn |

| 05/01/2024 | Vietstock Weekly 02-03/05/2024: Nhiều tín hiệu tiêu cực xuất hiện |

| 04/30/2024 | Chứng khoán phái sinh tuần 02-03/05/2024: Khối ngoại mua ròng mạnh |

| 04/29/2024 | Báo cáo TTCK thế giới quý 2/2024 (Kỳ 2): Nhịp điều chỉnh ngắn hạn đang hiện hữu |